Home Depot Faces Weaker Sales Momentum and Downgraded Outlook

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 5 hours ago

0mins

Should l Buy HD?

Source: stocktwits

- Weaker Sales Momentum: Stifel highlighted that Home Depot's recent sales data indicates weaker-than-expected comparable sales momentum, prompting the firm to lower its outlook for Q2 through Q4, reflecting a cautious stance on demand trends in the home improvement sector.

- Earnings Expectations: Analysts forecast Home Depot's Q1 revenue at $41.5 billion with earnings per share of $3.41, yet the company's stock has fallen over 14% in the past month, indicating market concerns regarding its performance.

- Structural Market Shift: With homeowners less likely to relocate due to high mortgage rates, Home Depot is accelerating its shift towards professional contractors, which is expected to play a crucial role in stabilizing comparable sales amidst weaker discretionary demand.

- Increased Competitive Pressure: Amidst economic uncertainty, Stifel has reduced Home Depot's price target from $375 to $320, reflecting concerns over consumer spending and housing activity signals, which may impact investor confidence.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy HD?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on HD

Wall Street analysts forecast HD stock price to rise

23 Analyst Rating

17 Buy

5 Hold

1 Sell

Moderate Buy

Current: 297.510

Low

320.00

Averages

401.47

High

441.00

Current: 297.510

Low

320.00

Averages

401.47

High

441.00

About HD

The Home Depot, Inc. is a home improvement retailer. It offers its customers an assortment of home improvement products, building materials, lawn and garden products, decor products, and facilities maintenance, repair, and operations (MRO) products, in stores and online. It also provides a number of services, including home improvement installation services, and tool and equipment rental. It operates over 2,359 stores located throughout the U.S. (including the Commonwealth of Puerto Rico and the territories of the U.S. Virgin Islands and Guam), Canada, and Mexico. Its stores average over 104,000 square feet of enclosed space, with over 24,000 additional square feet of outside garden area. It also maintains a network of distribution and fulfillment centers, as well as mobile applications and e-commerce websites in the U.S., Canada, and Mexico. It serves two primary customer groups, including both do-it-yourself (DIY) and do-it-for-me (DIFM) customers and professional customers (Pros).

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Home Depot Faces Weaker Sales Momentum and Downgraded Outlook

- Weaker Sales Momentum: Stifel highlighted that Home Depot's recent sales data indicates weaker-than-expected comparable sales momentum, prompting the firm to lower its outlook for Q2 through Q4, reflecting a cautious stance on demand trends in the home improvement sector.

- Earnings Expectations: Analysts forecast Home Depot's Q1 revenue at $41.5 billion with earnings per share of $3.41, yet the company's stock has fallen over 14% in the past month, indicating market concerns regarding its performance.

- Structural Market Shift: With homeowners less likely to relocate due to high mortgage rates, Home Depot is accelerating its shift towards professional contractors, which is expected to play a crucial role in stabilizing comparable sales amidst weaker discretionary demand.

- Increased Competitive Pressure: Amidst economic uncertainty, Stifel has reduced Home Depot's price target from $375 to $320, reflecting concerns over consumer spending and housing activity signals, which may impact investor confidence.

See More

Home Depot Reports Strong Q1 Earnings, Reaffirms 2026 Guidance

- Sales Growth Resurgence: Home Depot reported Q1 revenue of $41.8 billion, slightly exceeding analysts' expectations of $41.5 billion, with adjusted earnings per share of $3.43 beating the forecast of $3.41, indicating stable market demand.

- Strong Demand for Small Projects: While larger renovation projects faced weakness, the ongoing demand for smaller home improvement projects led to a 0.6% increase in comparable sales, reflecting consumer caution amid economic uncertainty.

- 2026 Guidance Reaffirmed: Home Depot expects total sales growth of approximately 2.5% to 4.5% for 2026, with comparable sales growth flat to 2.0%, and anticipates adjusted diluted earnings per share to increase by 0% to 4.0%, demonstrating confidence in future performance.

- Positive Retail Sentiment: On Stocktwits, retail sentiment around Home Depot remains 'extremely bullish', with message volumes in the 'extremely high' zone over the past 24 hours, reflecting market recognition and anticipation of the company's performance.

See More

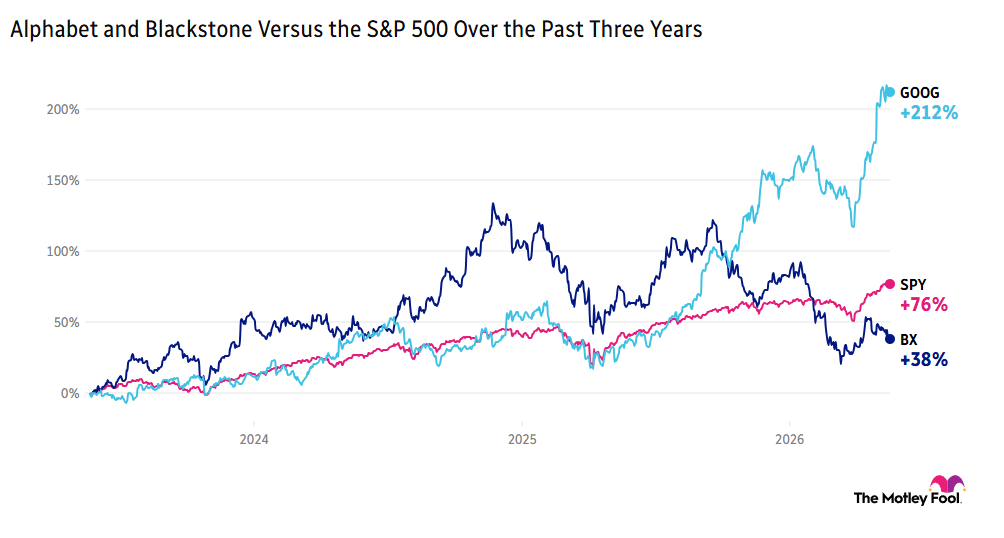

Alphabet and Blackstone Launch AI Venture

- AI Joint Venture Established: Alphabet and Blackstone have announced the formation of a new AI joint venture, with Blackstone providing an initial $5 billion investment aimed at meeting unprecedented demand for computing power, expected to deliver 500 megawatts of capacity, significantly enhancing market competitiveness.

- Data Center Asset Advantage: Blackstone currently holds over $150 billion in data center assets, and combined with Google Cloud's TPU technology, the new venture will offer robust data processing capabilities to clients, driving widespread adoption of AI technologies.

- Manufacturing Progress Notable: Intel's CEO stated that the foundry business is gaining traction, with monthly yield improvements of 7% to 8% exceeding expectations, showcasing Intel's potential as a high-margin revenue engine that could drive stock performance.

- Consumer Health Data Release: Home Depot rose 1% ahead of the opening bell, with U.S. pending home sales data expected to show a 1.5% month-over-month increase, reflecting resilience in the housing market and consumer confidence, further bolstering market sentiment.

See More

Home Depot Sales and Profit Beat Expectations

- Earnings Beat: Home Depot reported earnings of $3.43 per share, surpassing analysts' expectations of $3.41, indicating strong performance in the home improvement sector, which is likely to drive stock price appreciation.

- Revenue Growth: The company's revenue reached $41.77 billion, exceeding the market forecast of $41.52 billion, reflecting sustained consumer demand for home improvement products, which may encourage future investments and expansion.

- Sportswear Performance: Amer Sports reported first-quarter earnings of $0.38 per share, exceeding the FactSet estimate of $0.31, demonstrating brand competitiveness in the market and likely attracting more investor attention.

- AI Investment: Blackstone announced a $5 billion investment in a new AI infrastructure company in partnership with Google, boosting shares of both Blackstone and Alphabet by 0.7%, reflecting strong market confidence in the AI sector.

See More

Home Depot Q1 Earnings Beat Expectations

- Strong Earnings: Home Depot reported a non-GAAP EPS of $3.43 for Q1, beating expectations by $0.02, demonstrating the company's resilience amid economic uncertainty, despite a challenging overall market environment.

- Revenue Growth: The company achieved Q1 revenue of $41.8 billion, exceeding market expectations by $290 million, reflecting sustained consumer demand for home improvement and building materials, even under economic slowdown pressures.

- Market Challenges: While short-term market positions are affected by economic deceleration, Home Depot's long-term outlook remains optimistic, indicating the company's strategic capability to navigate market fluctuations.

- Industry Outlook: In the current economic climate, Home Depot may face challenges with declining remodeling and construction demand, but its robust financial performance lays a solid foundation for future growth.

See More

Home Depot Q1 Earnings Exceed Expectations

- Earnings Beat: Home Depot reported a non-GAAP EPS of $3.43 for Q1, exceeding expectations by $0.02, indicating the company's resilience in a challenging economic environment despite broader market headwinds.

- Revenue Performance: The company achieved Q1 revenue of $41.8 billion, surpassing the anticipated $41.5 billion, demonstrating relatively stable sales performance amid weakening demand in remodeling and construction sectors.

- Uncertain Market Outlook: While the short-term market conditions are tough, Home Depot's long-term prospects remain well-founded, reflecting investor confidence in the company's growth potential, particularly in the context of economic recovery.

- Industry Challenges: As economic slowdown intensifies, the remodeling and construction sectors face increasing market pressures, necessitating Home Depot to implement effective strategies to navigate these challenges and maintain competitive positioning.

See More

Home Depot Faces Weaker Sales Momentum and Downgraded Outlook

- Weaker Sales Momentum: Stifel highlighted that Home Depot's recent sales data indicates weaker-than-expected comparable sales momentum, prompting the firm to lower its outlook for Q2 through Q4, reflecting a cautious stance on demand trends in the home improvement sector.

- Earnings Expectations: Analysts forecast Home Depot's Q1 revenue at $41.5 billion with earnings per share of $3.41, yet the company's stock has fallen over 14% in the past month, indicating market concerns regarding its performance.

- Structural Market Shift: With homeowners less likely to relocate due to high mortgage rates, Home Depot is accelerating its shift towards professional contractors, which is expected to play a crucial role in stabilizing comparable sales amidst weaker discretionary demand.

- Increased Competitive Pressure: Amidst economic uncertainty, Stifel has reduced Home Depot's price target from $375 to $320, reflecting concerns over consumer spending and housing activity signals, which may impact investor confidence.

See More

Home Depot Reports Strong Q1 Earnings, Reaffirms 2026 Guidance

- Sales Growth Resurgence: Home Depot reported Q1 revenue of $41.8 billion, slightly exceeding analysts' expectations of $41.5 billion, with adjusted earnings per share of $3.43 beating the forecast of $3.41, indicating stable market demand.

- Strong Demand for Small Projects: While larger renovation projects faced weakness, the ongoing demand for smaller home improvement projects led to a 0.6% increase in comparable sales, reflecting consumer caution amid economic uncertainty.

- 2026 Guidance Reaffirmed: Home Depot expects total sales growth of approximately 2.5% to 4.5% for 2026, with comparable sales growth flat to 2.0%, and anticipates adjusted diluted earnings per share to increase by 0% to 4.0%, demonstrating confidence in future performance.

- Positive Retail Sentiment: On Stocktwits, retail sentiment around Home Depot remains 'extremely bullish', with message volumes in the 'extremely high' zone over the past 24 hours, reflecting market recognition and anticipation of the company's performance.

See More

Alphabet and Blackstone Launch AI Venture

- AI Joint Venture Established: Alphabet and Blackstone have announced the formation of a new AI joint venture, with Blackstone providing an initial $5 billion investment aimed at meeting unprecedented demand for computing power, expected to deliver 500 megawatts of capacity, significantly enhancing market competitiveness.

- Data Center Asset Advantage: Blackstone currently holds over $150 billion in data center assets, and combined with Google Cloud's TPU technology, the new venture will offer robust data processing capabilities to clients, driving widespread adoption of AI technologies.

- Manufacturing Progress Notable: Intel's CEO stated that the foundry business is gaining traction, with monthly yield improvements of 7% to 8% exceeding expectations, showcasing Intel's potential as a high-margin revenue engine that could drive stock performance.

- Consumer Health Data Release: Home Depot rose 1% ahead of the opening bell, with U.S. pending home sales data expected to show a 1.5% month-over-month increase, reflecting resilience in the housing market and consumer confidence, further bolstering market sentiment.

See More

Home Depot Sales and Profit Beat Expectations

- Earnings Beat: Home Depot reported earnings of $3.43 per share, surpassing analysts' expectations of $3.41, indicating strong performance in the home improvement sector, which is likely to drive stock price appreciation.

- Revenue Growth: The company's revenue reached $41.77 billion, exceeding the market forecast of $41.52 billion, reflecting sustained consumer demand for home improvement products, which may encourage future investments and expansion.

- Sportswear Performance: Amer Sports reported first-quarter earnings of $0.38 per share, exceeding the FactSet estimate of $0.31, demonstrating brand competitiveness in the market and likely attracting more investor attention.

- AI Investment: Blackstone announced a $5 billion investment in a new AI infrastructure company in partnership with Google, boosting shares of both Blackstone and Alphabet by 0.7%, reflecting strong market confidence in the AI sector.

See More

Home Depot Q1 Earnings Beat Expectations

- Strong Earnings: Home Depot reported a non-GAAP EPS of $3.43 for Q1, beating expectations by $0.02, demonstrating the company's resilience amid economic uncertainty, despite a challenging overall market environment.

- Revenue Growth: The company achieved Q1 revenue of $41.8 billion, exceeding market expectations by $290 million, reflecting sustained consumer demand for home improvement and building materials, even under economic slowdown pressures.

- Market Challenges: While short-term market positions are affected by economic deceleration, Home Depot's long-term outlook remains optimistic, indicating the company's strategic capability to navigate market fluctuations.

- Industry Outlook: In the current economic climate, Home Depot may face challenges with declining remodeling and construction demand, but its robust financial performance lays a solid foundation for future growth.

See More

Home Depot Q1 Earnings Exceed Expectations

- Earnings Beat: Home Depot reported a non-GAAP EPS of $3.43 for Q1, exceeding expectations by $0.02, indicating the company's resilience in a challenging economic environment despite broader market headwinds.

- Revenue Performance: The company achieved Q1 revenue of $41.8 billion, surpassing the anticipated $41.5 billion, demonstrating relatively stable sales performance amid weakening demand in remodeling and construction sectors.

- Uncertain Market Outlook: While the short-term market conditions are tough, Home Depot's long-term prospects remain well-founded, reflecting investor confidence in the company's growth potential, particularly in the context of economic recovery.

- Industry Challenges: As economic slowdown intensifies, the remodeling and construction sectors face increasing market pressures, necessitating Home Depot to implement effective strategies to navigate these challenges and maintain competitive positioning.

See More